Perhaps the most famous statistical fallacy is the gambler’s fallacy. To quote Wikipedia, the gambler’s fallacy is “the mistaken belief that if something happens more frequently than normal during a given period, it will happen less frequently in the future (or vice versa).” The canonical example of the fallacy is gamblers who reason that, since they haven’t lucked out recently, they’re more likely to get lucky in the near future — that is, that they are “due” for winnings.

Of course, sometimes it is very reasonable to believe that something will happen soon because it hasn’t happened for a while. For instance, if you’re drawing cards from a 52-card deck and haven’t noticed any aces yet, you’re more likely than average to encounter an ace soon. This is in contrast to flipping a fair coin, where if you’ve just flipped ten tails, there’s still only a

This brings me to the topic of this post: recessions. In ninth grade US history I remember learning about the business cycle. We learned that recessions happened “periodically” — every several years. I took this to mean that the pattern of recessions is somewhat predictable: if there was just a recession, a new one is unlikely; if it’s been several years, you should probably expect one soon. That is, a recession happening in a given year is a bit like an ace being drawn from a deck of cards, rather than like a coin coming up heads.

Was my teacher right that recessions happen periodically, or is this just a misconception stemming from the gambler’s fallacy? This is an important question that is consequential in the near-term: it’s been 122 months since the Great Recession ended, longer than any previous stretch of time between recessions. If recessions happen periodically, then we are likely due for one: even without looking at any economic data, we would think that there’s a higher-than-normal chance of a recession next year.

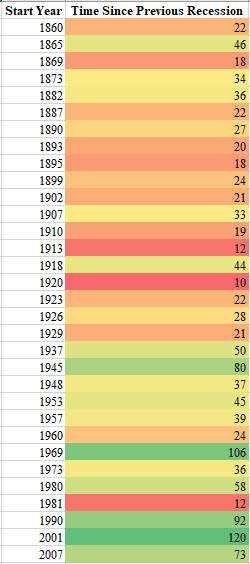

I decided to look at data of US recessions to try to answer this question. Below (taken from Wikipedia) is a list of years when a recession started and, for each recession, how much time passed since the end of the previous recession (in months).1

The first thing I noticed is that since the recession that began in 1929 (also known as the Great Depression) the average time periods between recessions have been much longer. Before the Great Depression, time periods between recessions were on average 25 months long; since the Great Depression, they have been 59 months long. I’m not sure why this is, but the effect is definitely there.2 For this reason I decided to look at the data in two chunks: before and after the Great Depression.

My goal was to see whether the stretches of time between recessions followed a predictable pattern. The antithesis of this hypothesis is that absolutely no such prediction can be made, i.e. that every month a new recession would start with some small probability

One property of exponential distributions is that if you draw some samples from the distribution, the standard deviation of the samples will usually be roughly equal to the mean. Indeed, on average the standard deviation divided by the mean will equal

On the other hand, imagine you believe that recessions become more and more likely the longer it’s been since the previous recession happened. Then you’d expect times between recessions to form a pretty narrow distribution: it would be rare to have very small or very large gaps between consecutive recessions. In other words, you’d expect the standard deviation to be substantially less than the mean (so their ratio would be substantially smaller than

In the data above, before the Great Depression, the standard deviation of the data divided by its mean was

On the other hand, after the Great Depression, the standard deviation of the data divided by the mean is

The conclusion that I’m comfortable coming to is that it’s probably still the case that recessions are more likely to happen if it’s been a while since the previous recession. If we only had post-Depression data, I’d probably not be comfortable drawing that conclusion, but we already have priors (stemming from the pre-Depression data) that recessions are predictable.

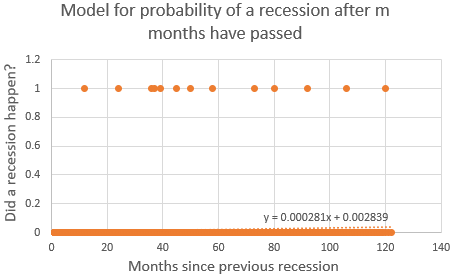

So when can we expect another recession? I made a quick-and-dirty model to answer this question: for every month between recessions since the Great Depression, I plotted a point whose x-value was the number of months since the previous recession and whose y-value was

The answer I got was that around now (September 2019), the probability of a recession starting each month is around

If this model is accurate, the expected time to the next recession is about two years. This accords fairly well with my intuition.

So, what does this all mean in light of the recent reporting that a recession has gotten more likely in the near future? Here’s my take:

- Even before we got other indications (e.g. the yield curve inversion), we should have probably been expecting a recession to come soon.

- A recession would probably be happening around now or soon regardless of actions by the federal government, whether it be Trump’s trade policies or the Fed’s monetary policy. Consequently it would be unfair to blame Trump or the Fed (or Congress) for a recession without substantial additional evidence.

- But a caveat: just as there was a shift in recession frequencies after the Great Depression (perhaps as a result of changes in fiscal and/or monetary policy), there may have again been a shift in recession frequencies following the Great Recession. So perhaps the long recession-less period since the Great Recession is indicative of a new normal.

[Thanks to Mike Winston for suggesting the standard deviation divided by the mean as a statistic to test for significance and for suggesting how to model the monthly probability of a recession happening.]

1. A recession is defined as a time period in which the GDP shrinks for two consecutive quarters.↩

2. I ran a two-sample t-test and got a p-value of 0.3%. That is, if we assume that any difference in average time period between recessions before and after the Great Depression is due to random noise, the probability of getting such a stark difference is only 0.3%. This value is low enough that I’m confident asserting that the difference is not just by chance.↩

One thought on “Are we due for another recession? Probably.”