There have been tons of takes and articles written about GameStop. The vast majority are really wrong, and most of the good ones assume a lot of background. This post is my attempt to provide an explanation of what happened without assuming any background. This necessarily involves lots of simplifications (so if I get something wrong, it’s possible that that’s out of ignorance, or that I’m leaving out details I’ve judged unnecessary); but if you think I’ve gotten something wrong in a way that’s misleading to the overall points I make, leave a comment below!

Ultimately, the question I want to answer is: many investors lost a lot of money to the GameStop bubble; how sad is this, and who bears responsibility? But before I do that, I’ll need to give some background on the stock market, what it’s for, and how it works. Obviously feel free to skip around if you already have background.

Background: The big long

(See this excellent article by Matt Levine for a more thorough summary of what I’m saying here.)

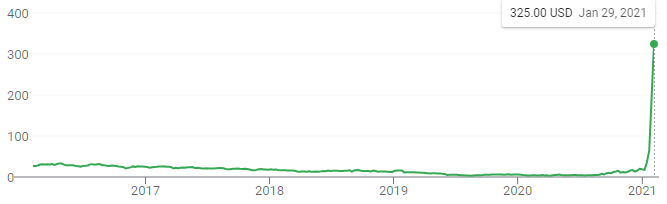

This is a chart of the stock price of GameStop (stock symbol: GME), a company that sells various kinds of games, mostly video games. It was worth about $5 per share for most of 2020. There’s about 70 million shares of GameStop, so the whole company was worth about $350 million.

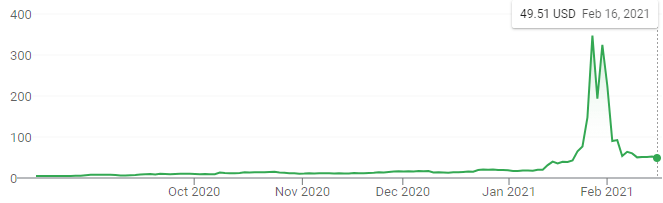

On January 29th, GameStop’s stock closed at $325 (it traded as high as $483). That translates to a market value of 23 billion dollars. (It has since declined to $50 — we’ll get to that.)

So, what happened? Did GameStop suddenly get a massive influx of people wanting to buy its games? Did it secure some super lucrative contract? Nope, nothing like that.

Maybe you already know the story, but let me summarize it briefly. There is a subreddit called r/WallStreetBets (CW: crude language, slurs). As I’m writing this, it has 9.1 million users. The basic idea of the subreddit is: people post amateurish analyses of stocks, other people read those analyses, and then maybe buy or sell shares. Sometimes they coordinate to all buy shares of a company just for fun. Essentially it’s a community of people that are having fun together by gambling on the stock market and making memes about it all.

Recently, the denizens of r/WallStreetBets decided to buy huge amounts of GameStop stock, and in doing so they created a short squeeze. Simplifying considerably, an unusually large number of investors (these are mostly not the r/WallStreetBets people) had sold the stock short. Here’s what that means: let’s say that Sharon the Short Seller thinks that GameStop is overvalued and wants to make a bet that its share price will go down. If Sharon had any GameStop shares, she would have sold them, but she doesn’t. So instead, she borrows some shares of GameStop from Ingrid the Investor (for a fee), and sells them. Later, Sharon buys back the stock and gives it back to Ingrid. If her prediction was right and the price went down, she will have bought the stock back for cheaper than she originally sold it, and will have made a profit. If she was wrong and the price went up, she will have lost money.

But, what if the price of GameStop goes way up? At that point, Ingrid might get concerned: what if the share price will keep going up, and eventually Sharon won’t have the money to buy back the shares she lent from Ingrid and then sold? So Ingrid tells Sharon to buy the shares back now. And the way that short selling works, Sharon has to comply, even if she doesn’t like the price.

Now, the fact that Sharon has to urgently buy back a bunch of shares drives the price up (since there’s more demand for shares). At this point, other people in Ingrid’s position demand their shares back (because they get concerned, just like Ingrid did), the price rises even more, yet more investors demand their shares back, and so on. This is called a short squeeze.

A short squeeze can drive a share price up pretty dramatically. In 2008, one caused Volkswagen’s share price to increase nearly five-fold. This briefly made Volkswagen the most valuable company in the world!

But, Volkswagen’s share price went up only five-fold. Meanwhile, GameStop’s share price increased by a factor of more than 50! GameStop is more vulnerable to such dramatic moves because it’s pretty small, but this is nonetheless impressive.

Now, my understanding is that the push in r/WallStreetBets to buy GameStop did not originate with the primary goal of creating a short squeeze. Matt Levine writes:

This is fun, a nice social outing in an age of social distancing, a risky but potentially lucrative collective entertainment. Recently they decided to do GameStop. Because, I don’t know, they’re gamers, or because it’s a little comical to pump the stock of a chain of mall video-game stores during a pandemic, or because a lot of professional investors are short GameStop and they thought it’d be funny to mess with them. Or, especially, because their friends on Reddit were buying GameStop and they figured they’d join in the fun. Or all of those things in different combinations. Take one person who’s long for fundamental reasons, add 100 people who are long for personal-amusement reasons like “lol gaming” or “let’s mess with the shorts,” and then add thousands more who are long because they see everyone else long, and the stock moves.

However, as the prospect of a short squeeze became viable, “messing with the shorts” became a primary motivation. Quoth John Authers:

Instead of greed, this latest bout of speculation, and especially the extraordinary excitement at GameStop, has a different emotional driver: anger. The people investing today are driven by righteous anger, about generational injustice, about what they see as the corruption and unfairness of the way banks were bailed out in 2008 without having to pay legal penalties later, and about lacerating poverty and inequality. This makes it unlike any of the speculative rallies and crashes that have preceded it.

So WallStreetBets’ mantra isn’t just “lol gaming”, it’s also “let’s make the hedge funds pay”. Don’t take it from me, or from John Authers; take it from a strongly upvoted post on the subreddit:

To Melvin Capital: you stand for everything that I hated during [the 2008 financial crisis]. You’re a firm who makes money off of exploiting a company and manipulating markets and media to your advantage. Your continued existence is a sharp reminder that the ones in charge of so much hardship during the ’08 crisis were not punished. And your blatant disregard for the law, made obvious months ago through your (for the Melvin lawyers out there: alleged) illegal naked short selling and more recently your obscene market manipulation after hours shows that you haven’t learned a single thing since ’08. And why would you? Your ilk were bailed out and rewarded for terrible and illegal financial decisions that negatively changed the lives of millions. I bought shares a few days ago. I dumped my savings into GME, paid my rent for this month with my credit card, and dumped my rent money into more GME (which for the people here at WSB, I would not recommend). And I’m holding. This is personal for me, and millions of others. You can drop the price of GME after hours $120, I’m not going anywhere. You can pay for thousands of reddit bots, I’m holding. You can get every mainstream media outlet to demonize us, I don’t care. I’m making this as painful as I can for you.

But, GameStop’s share price couldn’t stay this absurdly high forever. Since then, the price has declined to $50, and I would guess that it will go down some more. This means that many retail investors (i.e. random individuals) have lost a lot of money and may lose even more, and that’s really sad.

So, what to make of all this? Who is responsible for all this mess? The hedge funds? WallStreetBets? Capitalism? To paraphrase Harry Truman, where does the GameStop buck stop?

Why even the stock market?

To discuss this question intelligently, it’s first necessary to understand why the stock market exists. So, what is the point of the stock market anyway?

Imagine that you run a startup. Maybe your startup builds cheap car batteries. Maybe it efficiently synthesizes important chemicals. Maybe you’re working on AI chat bots.

In order to run your startup, you need money. Maybe you need to build a factory for building your batteries. Maybe you need to acquire fancy lab equipment to run your synthesis reactions. Maybe you need to hire software developers and machine learning experts.

So far, you have been solving your problem with private investors. Basically, you’ve been going up to rich people and explaining why you think your startup will be successful. Some of them have been persuaded and have offered to give you money in exchange for a share of your company’s future profits. That is, you need money now; the rich people have money, and they are betting that your startup will be successful and bring in even more money than they’re giving you now. It’s a win-win: you’re able to run your company, and they’re hoping for a return on their investment.

But lately things haven’t been going great. This could be for a number of reasons:

- Your startup is big enough that you’re having trouble finding investors who will give you enough money.

- Your current investors — who may have substantial influence over your company’s decisions as part of the investment contract — want to sell their share of the company (perhaps because they want to make other investments instead), but can’t find enough buyers.

- The process of finding new investors is arduous and takes away resources from actually developing your company.

One thing you can do is take your company public. Roughly speaking, the way this works is: you talk to a bunch of big banks and tell them everything about your company. They do their best to figure out how much your company is worth, and then offer to buy shares of your company at what they believe is a fair price. Then, your company gets listed on the stock exchange, and traders — everyone from big banks to hedge funds to your uncle — can freely trade shares of your company.

(Why are the big banks willing to buy shares of your company even though you had trouble finding investors earlier? It’s precisely because your company is about to be listed on the stock exchange: this reassures banks that they can offload their shares whenever they feel the time is right, which private investors generally can’t do.)

In other words, the stock market makes it much easier for big companies to raise money. If your company wants to raise more money in the future, it can sell more shares directly into the stock market.1 Or, more commonly, it will ask for a loan (either from a big bank, or issue bonds which can then be traded on a bond market). Getting loans is much easier if your company is publicly traded, because that makes it a lot easier for lenders to appraise the company. So basically, the stock market facilitates mutually beneficial exchanges between companies and potential lenders/investors by lowering the amount of friction involved in investing or lending (e.g. by allowing investors to sell their shares whenever they want and by giving lenders access to more information).

Stock prices

Stock prices are kind of confusing: what does it mean about a company if its one billion shares are worth $10 each?

What does a stock price represent?

The answer is something like: the expected future earnings of the portion of the company corresponding to one share. If there are 1 billion shares of a company and each share is worth $10, this means that one-billionth of the company’s expected future earnings is $10. This isn’t quite accurate, for a number of reasons: money now is worth more than money later, so earnings in the far future count for less; investors are generally risk-averse, so the market value of a company (the dollar value of all its shares) is less than its expected (time-discounted) future earnings by an amount corresponding to how much uncertainty there is about the earnings; and there are various other caveats. But for the most part you can think of it as “expected future earnings”. When a hedge fund buys shares of a company, it’s usually expressing the belief that the company will have higher future earnings than its share price implies. When it sells (or short sells) shares, it’s usually expressing the opposite belief. If the hedge fund is right, it will eventually make money off of the bet.

When you own shares of a company, you are usually paid out dividends, i.e. your fair share of the company’s recent earnings. To a first approximation, the price of a share reflects the total dividends that the company is expected to pay out on that share over the company’s lifetime (again, time-discounted and adjusted for risk).

What mechanisms keep stock prices in line with reality?

(Here, “reality” means “the company’s future earnings”, modulo the aforementioned caveats and adjustments.)

The easy answer is “if a company’s share price is undervalued (or overvalued), people can buy (or sell) the shares, eventually making money when the share price returns to being reasonable”. But this argument presupposes that stock prices reflect reality in the long term; why would that be the case?

In my mind, the main reason is dividend payments. If the price of a share is too low, there is money to be made by buying shares of the company and just keeping them around, accumulating dividend payments. Likewise, if the price of a share if too high, owners of the company’s shares can make money by selling their shares, since the total dividend payments they should expect to get is less than the market value of the shares they own.2

There are a few other things that keep a company’s share price in line. One is selling more shares (where the company offers shares at market value in exchange for cash) or, conversely, stock buybacks (where the company buys back its own shares, giving back investors their money). These tools are generally used if (in the case of offerings) the company feels that it could use more cash effectively, or (in the case of buybacks) it has money it doesn’t know what to do with; but they can also be used if the company feels that its share price is too high or (respectively) too low.

Is it bad for the world if a stock price isn’t in line with reality?

I would argue that the answer is yes. The basic reason for this is that stock prices guide the allocation of financial resources. Concretely:

- Companies can sell additional shares on the market, thereby raising more money to finance operations. If a company is undervalued, that likely limits the amount of money it would be able to raise (since the amount of money that market participants would be willing to give the company is probably roughly proportional to the company’s market value). Conversely, if a company is overvalued, it can raise too much money by selling shares. (AMC did just that when the people of r/WallStreetBets decided to drive its price up a bunch.) This is probably bad, because a likely counterfactual is that other companies — which are properly valued and could use the marginal dollar raised more effectively — would have gotten the money instead.

- Banks take the market value of a company into significant consideration when deciding how much money to loan to the company. The reason for this is straightforward: a 100 billion dollar company it much more capable of paying back a billion dollar loan than a 10 billion dollar company. This means that if a company is undervalued, it’s artificially hard for it to get a loan, inhibiting future growth. If a company is overvalued, it is artificially easy for the company to get a loan. Again, this is probably bad because if Company A gets a large loan because it’s overvalued, this means that some other Company B gets a smaller loan as a result, since banks aren’t willing to loan out unlimited amounts of money. Meanwhile, B could have probably used that marginal money more effectively than A.

The other thing to keep in mind is that share prices that are out of line will probably come into line with reality eventually. People who invested in a company while its share price was too high will lose a lot of money. Likewise, people who invested in a company while its share price was too low will gain a lot of money — so basically, having stock prices that don’t represent reality adds unnecessary risk for investors, which would (rightly) make people more reluctant to invest, making it harder for companies to raise money and expand their operations, etc.

What impacts do short sellers have on the stock market?

This is a hard question. Here’s a good article on the matter by Noah Smith; as is his style, he first lays out the answer given by economic theory and then discusses to what extent empirical evidence justifies the theory.

Here’s the theory, as Smith lays it out:

If you don’t allow short-selling, then it could be hard to correct overvaluation. Suppose Facebook stock is at $300 a share. And suppose half the people (let’s call them the “realists”) realize that Facebook is only worth $200 a share, and half are just crazy bullish and incorrectly think it’s worth $500 a share. Do their opinions just sort of cancel out? Well, no. Sure, the realists could push the price down by selling shares — if they had any. But remember, the realists think FB is overvalued at $300, so maybe they don’t actually own much of it, because why would you own an overvalued stock? Instead they already offloaded it to the optimists, who eagerly paid higher prices for it. Now the optimists own all the stock, and there’s no way to get the price back down to $200 by selling it.

Enter short-sellers. They borrow FB shares (from the optimists) and sell those shares, pushing the price down. Then in a little while when all the optimists wake up and realize that FB is really only worth $200 a share, and the price goes down, the shorts can buy the stock back for the cheaper price, return the shares to whoever they borrowed it from, and pocket the difference. That is how shorts make money.

Without short-sellers, it’s theoretically very hard to push stock prices down past a certain point. Many economic theorists have argued that this tends to lead to persistent overvaluation in the market. Without shorts, they predict, prices will be higher than fundamentals.

Some economists even think that short-sellers can pop stock bubbles, or prevent them from getting started. Maybe when prices rise because of a burst of optimism, it gets everyone’s attention and causes some people to think the rising prices are a new trend, so they all buy in and push the price to the moon🚀🚀🚀! Then the crash comes and regular folks lose their life’s savings to the savvy hedge funders who knew exactly when to time the top. But with short-sellers around, maybe that bubble would never get started, and normal people wouldn’t lose their life’s savings to savvy market-timing hedge funds, because they wouldn’t have seen that initial price rise to begin with.

This mostly makes sense to me. I would add, though, that I wouldn’t expect the overvaluation to be uniform across different companies. In particular — and this is just my guess — I would expect companies that have a lot of hype (like Tesla) to be much more overvalued than boring companies (Visa, say). I imagine there isn’t all that much short-selling to be done by pushing back on hordes of over-excited Visa investors; Tesla is another story.

Okay, so that’s the theory. What about practice?

Sometimes policymakers ignore the economists and ban or restrict short-selling anyway. And this allows economists to study what actually happens when you ban shorting. It turns out that short-selling bans are not quite as important as you might think.

For example, when Australia banned short-selling in the wake of the Global Financial Crisis, it made stock prices a bit more volatile, and made trading a bit more expensive, but it didn’t actually boost prices. Another study around the world from the same period found the same thing — bans on short-selling made stocks more volatile and more expensive to trade, but they didn’t actually make prices higher!

My sense is that the two studies linked are not entirely representative. Here’s a quote from the second study:

Since the predictions of the theory regarding the effect of short sales on stock prices are ambiguous, the verdict is essentially entrusted to empirical studies. Jones and Lamont (2002), who use detailed data about shorting costs in the New York Stock Exchange (NYSE) from 1926 to 1933, find evidence consistent with the overpricing hypothesis. Chang, Cheng, and Yu (2007) address a similar research question using data from the Hong Kong stock market, where only stocks on a list of designated securities can be sold short: the addition of individual stocks to the list tends to cause stock overvaluation, with more dramatic effects for individual stocks with wider dispersion of investor opinions. In contrast to these findings, however, research on the suspension or complete removal of short-sale price-tests such as the uptick rule in the U.S. finds no significant stock price effects (e.g., Diether, Lee and Werner, 2009; Boehmer, Jones, and Zhang, 2008).

Their description of the Hong Kong study seems pretty compelling: on the Hong Kong stock market, only some stocks are allowed to be sold short. This allows researchers to see what happens when a stock is added to or removed from this list. Apparently short sale bans lead to “dramatic” overvaluation effects! (The above quote contains a typo that makes it sound lik the effect is in the other direction, but it is in fact in the direction predicted by the theory; see here for the original study by Chang, Cheng, and Yu.)

So my (weak) sense is: if short selling is banned for particular stocks, those stocks end up substantially overvalued; if short selling restrictions or bans are placed on the market as a whole, there’s either no overvaluation effect or a mild one. Though my best guess is that “no overvaluation effect” really means “no net overvaluation effect”, with some (e.g. overhyped) stocks being overvalued, while others are undervalued.

Short sellers likely do more than just keep prices at reasonable levels: there is a decent amount of evidence that short sellers decrease the bid-ask spread. What this means is: the price to buy a share is never the same as the price at which you can sell it. For instance, you might be able to buy a share of a company for $10.05 (this is called the “ask price”), but you can only sell it for $9.95 (this is called the “bid price”).3 In this case, the bid-ask spread is 10 cents, and what this means is that if you want to buy (or sell) a share of this company, you’ll need to pay 5 cents extra per share. Not a ton, but not nothing either! There is evidence that the presence of short sellers decreases this spread, meaning that you don’t need to pay as much of a premium.

In summary, short sellers likely provide a valuable service by keeping market prices in line with reality, decreasing volatility, and narrowing the bid-ask spread. I have a medium amount of confidence in this conclusion.

So what does this mean for the GameStop saga?

Since GameStop’s peak at $483, it has dropped by a factor of 10 to around $50.

This means that tons of people who heard about the GameStop hype around January 30th and decided to invest have lost almost their entire investment. Some of these are frequenters of r/WallStreetBets who knew what they were getting into. But others were innocent investors who knew little about the stock market and got caught in the fray.

I don’t believe that — on the whole — hedge funds who were shorting GameStop did anything morally wrong. Instead, they were playing their role in a system that benefits the world by keeping markets efficient (as we’ve discussed). Hedge funds who were shorting GameStop after the craze had begun were providing a particularly valuable service by keeping prices less crazy than they would have been otherwise, despite the risk of losing tons of money in a short squeeze. They’ve been handsomely rewarded for this service as the share price has declined, which makes a lot of sense: prices got so high because not many hedge funds were willing to take on the risk they took on. Those who took on the huge risk got a correspondingly huge reward.4

(There’s some nonsense on the internet about how, because the short interest was over 100%, hedge funds “promised to buy more shares of GameStop than actually existed” or whatever. This is wrong because if e.g. there are 10 million shares and 15 million are sold short, then investors collectively own 25 million GameStop shares, more than the 15 million that have been sold short. See here for a more detailed explanation.)

(Now, this isn’t to say that there were no bad actors among the short sellers. In particular, the practice of naked short-selling has come under scrutiny; I don’t really have an opinion on whether naked short-selling is bad, but it might be. But I don’t think short sellers as a whole acted inappropriately.)

On the other hand, I do believe that posters on r/WallStreetBets acted inappropriately. They decided to wage a war against short sellers, knowing full well that if they succeeded, many investors would lose a lot of money as collateral damage. The result was a redistribution of wealth — not from hedge funds to retail investors, but from some retail investors (who got lucky and either bought when GME was low or sold when it was high) to other retail investors (who got unlucky and either sold low or bought high). Random redistributions of wealth are bad! A world where everyone has $100k is better than a world where half have $50k and half have $150k. But in fact this was a net-negative redistribution for retail investors: I strongly suspect that Wall Street firms made quite a bit of money off of all this.

So I guess in my ideal world, the innocent, uninformed retail investors would have ended up making some money off of the r/WallStreetBets investors who were buying up GameStop for the memes and the war, perhaps with hedge funds and other firms taking a small cut for their service of providing liquidity. But I imagine what happened was much worse: people on r/WallStreetBets who started this whole thing made a bunch of money, while innocent investors who bought from them near the peak lost a bunch of money.

How much money? It’s really hard to tell, but over a hundred billion dollars of GameStop stock traded over the past few weeks, a large chunk of it from retail investors. So, I would guess that the net redistribution amounts to billions of dollars, which is a lot.

(Matt Levine points out that there haven’t been anecdotes in the mainstream media of people losing their life savings betting on GameStop, and I imagine that journalists are looking for these anecdotes, so maybe there aren’t many such people. On the other hand, if I just lost my life savings on GameStop I probably wouldn’t be seeking out media attention. So I’d guess that there are tens but not hundreds of such people, but hundreds of thousands of people who lost (merely) thousands of dollars to the bubble.)

But overall, my judgment is that r/WallStreetBets waged an unjust war, many retail investors got caught in the fray, and the world is worse as a result. I have a medium to medium-low amount of confidence in this conclusion. (My main sources of doubt are about things I haven’t taken into consideration. For example, maybe the primary effect will be that more people will invest in the stock market in the future.)

What about Robinhood?

Robinhood is an app that lets people trade stocks for free. (How does it make money? This is pretty interesting — see footnote.5) For a couple of days in late January, it substantially restricted its users’ ability to trade shares of GameStop and some other stocks that were being pumped by r/WallStreetBets. People were very unhappy with this move — so much so that (as I write this) Robinhood now has a 1.4 star rating on the Google Play Store.

There are various conspiracy theories saying that Robinhood did this to benefit Citadel, a hedge fund, in exchange for something or other. This, as far as I can tell, is nonsense. Robinhood’s explanation is that it was required to do so by its clearinghouse; basically, had Robinhood not restricted trading, it would have taken on an unhealthy amount of risk, which could have led to a situation where it owed its users GameStop shares that it did not have the financial resources to buy. (This can happen because, for logistical reasons, Robinhood cannot immediately buy the shares that its users request.) I don’t see a reason to disbelieve them — especially given that lots of other trading platforms did the same thing.

Of course, Robinhood wouldn’t have done this if it weren’t legally required — which is a shame! I think it was really good for the world that this happened, because it reduced the number of retail investors who ended up getting screwed over by the GameStop bubble.

This is not to say that Robinhood is blameless for the GameStop bubble. On the contrary, I’m inclined to put a fair amount of blame on Robinhood: its interface makes trading feel like a game, likely causing more of this sort of uninformed gambling. But I don’t think the fact that they curtailed trading was bad. People are mad at Robinhood for the wrong reasons.

In conclusion…

This saga didn’t end up changing my opinion of big institutions such as hedge funds and Robinhood, but it did substantially lower my opinion of r/WallStreetBets. I no longer think of them as silly memesters, but as a large entity capable of coordination that can do real harm. I’m not really sure how to fix this. I don’t think Reddit should ban them, since I can’t articulate a meta-level principle that I would endorse under which they would be banned. I also don’t think that the SEC should take action against random Redditors who participate in a short squeeze like the one we just saw. On the other hand, it may make sense for the SEC to go after the really influential Redditors who know better than to orchestrate short squeezes and pump-and-dump schemes. Again, though, I’m not really sure. I guess I’m mainly hoping that this whole thing blows over, institutions adapt, and not too many people end up getting hurt. I’d also like to see some regulation of entities like Robinhood which are getting people addicted to stock market gambling — but again, I’m not sure what sorts of regulations would be appropriate.

1. The mechanics of this took me a while to wrap my head around, so here’s an example. Say that a company is entirely publicly traded; say it’s worth $10B and has 100 million shares outstanding (worth $100 each). It can then issue a secondary offering of 10 million additional shares, at a price of (around) $100. That means it’s asking people to invest an additional billion dollars into the company (in exchange for future returns paid out as dividends, as usual). If it manages to sell those shares, it will now be worth $11B: the original $10B plus a new $1B in cash (which it can then use to buy new equipment, hire new workers, etc.). The original shareholders don’t become richer or poorer as a result: they have whatever shares they had originally, which are still worth $100 each.↩

2. But by holding onto the shares, won’t you be getting the dividend payments in addition to however much the shares will be worth many years from now? Yes, but however much the shares are worth many years from now represents the total dividends that are still to be paid out by the company. Eventually the company will go bankrupt, or be acquired, or fade into insignificance, etc., at which point most of the value you will have gotten from owning its shares will have been the dividends it had paid out.↩

3. The reason for this spread is that no one is willing to offer a share for less than $10.05 or bid more than $9.95 for a share, for fear of making a bad trade against a more knowledgeable counterparty.↩

4. A tangential point: should hedge fund profits be taxed more? Maybe; I have no clue. But I strongly suspect that the more you tax them, the larger the market inefficiencies you’ll end up having, since correcting some inefficiencies will no longer be worth the risk. So it’s not just a matter of optimally redistributing wealth (if that were the only consideration, you’d probably want to tax hedge funds a ton); there is a real cost to be paid in terms of market efficiency, and these are the sorts of trade-offs that policy analysts should evaluate.↩

5. Orders on the stock exchange are typically anonymous. But imagine you’re a hedge fund; if you see an offer on the market that you might want to take, do you care who is making that offer? The answer is yes! If another hedge fund is making the offer, then they might be more informed than you, so you might be making a bad trade. But if the offer is being made by someone like Robinhood, who just needs to buy shares for its users, they aren’t particularly price sensitive so you’re probably fine making the trade. This allows for the following deal: hedge funds (such as Citadel) pay Robinhood to make trades privately with them, so that they know that they are trading with Robinhood. Everyone ends up better off: the hedge funds (because they make profitable trades), Robinhood (because they get paid by the hedge funds), and the retail investors who use Robinhood (because hedge funds are willing to fill Robinhood’s bids and offers at better prices if they know that those bids and offers are coming from Robinhood). See this post for a more detailed explanation (h/t simon).↩

I’m a little bit confused as to why you wrote this (and I’m a little bit unsure as to whether it’s worthwhile commenting on). There have been so many GME takes already and yours doesn’t seem to add anything. I’m guessing it’s mostly in the hope that you could be corrected for the bits you’ve misunderstood, so I’ve quoted a bunch of bits which stuck out. This is by no means exhaustive and I broadly disagree with most of your conclusions.

* “Later, when she wants, Sharon ..” actually, the mechanics of short selling generally means that it’s not “when she wants” in the same way that if you own shares you can choose when to sell them. When you’re short something, the borrow is generally for a specified period of time. People tend not to think carefully about the mechanics of this (because most of the time it doesn’t matter) but when the borrow disappears you have to buy back the shares. You don’t have a choice. “Ingrid might get concerned…” again, you’ve not quite understood the mechanics here. Short sellers have to post margin. The people who lend the shares are not (generally) worried about not being paid back since they have collateral. The short seller is generally the person who is concerned because they are losing boatloads of cash.

* (From [1]) “The original shareholders don’t become richer or poorer as a result: they have whatever shares they had originally, which are still worth $100 each”. This is half-right. This is only true if the company issues shares at exactly the fair price. If they issue shares too cheaply the original shareholders have lost out.

* ““High liquidity” is a fancy way of saying “low bid-ask spread”, though there are other measures of market liquidity” No, it really isn’t.

* “I don’t believe that — on the whole — hedge funds who were shorting GameStop did anything wrong.” Sure, I think I broadly agree with this, although I think this section is avoiding the relevant point. HF shorting >$100 were generally doing nothing wrong and I’m sure they sized their positions appropriately and we rewarded. The funds who were short during the early run-up and got taken to the cleaners absolutely made some pretty dire mistakes. I think conflating those two actors is a mistake.

* “There’s some nonsense on the internet about how…” there is a lot of nonsense there, but I think you are also missing the bigger picture. 100% isn’t a magic number, but it is a very high short interest and that is absolutely a red flag when looking at a company.

* ” In particular, the practice of naked short-selling has come under scrutiny” I’ll throw my 2c in and say that I think naked short selling in the form which is actually used is a complete red herring and related to a topic which you broadly avoided talking about. Market making.

* “while innocent investors who bought from them near the peak lost a bunch of money.” This section manages to neatly walk around the fact that retail were NET SELLERS during the crazy overvalued period.

* “my judgment is that r/WallStreetBets waged an unjust war, many retail investors got caught in the fray” I think this is fairly unlikely to be the right take, for reasons which I don’t especially fancy going into.

* “This allows for the following deal: hedge funds (such as Citadel) pay Robinhood to let them know which bids and offers are Robinhood’s, so that they can trade with Robinhood without worrying about being ripped off. (In practice they probably make these trades privately.)” The bit in brackets is correct. The first section is not correct. In fact, that would be horribly illegal and terrible for the retail investors.

* A better version of [5] would be Patrick McKenzie’s post (https://kalzumeus.com/2019/6/26/how-brokerages-make-money/)

LikeLike

Thanks for the thoughts. I’ve edited my post somewhat in light of your comment. But overall I feel like the things you point out aren’t so much fundamental misunderstandings as simplifications that (I think) don’t get in the way too much — though I could be wrong. Replies point by point:

* “I’m a little bit confused as to why you wrote this (and I’m a little bit unsure as to whether it’s worthwhile commenting on). There have been so many GME takes already and yours doesn’t seem to add anything.” I haven’t seen any takes that I’ve liked that try to explain things from scratch. I’ve seen takes that explain things from scratch *completely incorrectly* and also takes that assume a lot of background from the reader.

* “Mechanics of short selling”: Yeah, I realize that there’s a borrow period. However, if I understand it correctly, this isn’t usually an important fact, because Sharon can just re-borrow (paying more interest). If things get weird then the precise borrow period can be important, but I’m not sure that fact is important for what’s going on here (I could be wrong). Also — I realize short sellers have to post margin, but the margin they post isn’t infinite. If I short a share for a dollar, it looks like I’d have to post a margin of $1.50, which would mean that Ingrid is in a bad spot if the price rises to above $2.50. Have I misunderstood?

* “This is half-right. This is only true if the company issues shares at exactly the fair price. If they issue shares too cheaply the original shareholders have lost out.” True, though don’t they have an incentive *not* to issue shares too cheaply, since they are happier raising more money than less? Also, wouldn’t this violate their fiduciary duties?

* “““High liquidity” is a fancy way of saying “low bid-ask spread”, though there are other measures of market liquidity” No, it really isn’t.” I’m not really sure what to do with “no, it really isn’t”, given that you don’t elaborate. I realize there are lots of measures of liquidity, but bid-ask spread is totally one of them. And in fact it’s the measure used by the paper I quote, so I feel pretty justified here.

* “The funds who were short during the early run-up and got taken to the cleaners absolutely made some pretty dire mistakes.” Oh, to clarify, by “didn’t do anything wrong”, I meant “didn’t do anything *morally* wrong”. They certainly made *strategic* mistakes. I could see an argument that making strategic mistakes is immoral, but I think it’s the sort of immoral that you’re strongly incentivized not to make, so when you make it, it’s probably a stupid mistake rather than an evil mistake.

* “100% isn’t a magic number, but it is a very high short interest and that is absolutely a red flag when looking at a company.” Yeah — a very high short interest makes a short squeeze much more possible — but the point that the nonsense I’ve seen purports to make is that hedge funds were doing something *immoral* by driving up the short interest that high (generally they treat 100% as a magic number, but even if they didn’t, I don’t see why it would be immoral to short sell when lots of other people are short selling).

* “Market making.” What do you think I should have said about market making?

* “Retail were NET SELLERS during the crazy overvalued period.” What’s your source? If it’s the Matt Levine article I linked to when I wrote that a large chunk of the trading was from retail investors, then I have two responses. First, they (or at least the portion that went through Citadel) was 50.2% sellers — so basically flat. Second, I bet this would change if you include the week leading up to the crazy week, which had almost as much volume as the crazy week.

I’m not sure what a good model is, but here’s my rough guess:

– In the week before the crazy week, the people who were “in the know” — active on r/WSB etc. — bought GME shares, mostly from hedge funds.

– In the crazy week, retail investors bought and sold roughly equal amounts of GME, as did hedge funds + market makers. My best guess about how this shook out is that retail investors who bought in the prior week net sold during the crazy week, and that new (probably less informed on the whole?) retail investors net bought. Hedge funds and market makers probably made a lot of money by buying low and selling high.

My main point is that there was a lot of *redistribution* of wealth, not that retail investors *net lost money* (I think it’s likely but not certainly true that they net lost money). And my guess is that the redistribution was from less informed players to more informed players, which in this case is the sad direction imo.

(Edit: I also left options out of the discussion, so as to not make things too complicated. I’m wondering whether retail investors were net buyers of call options — and if so, which ones — during the crazy week.)

* “The bit in brackets is correct. The first section is not correct. In fact, that would be horribly illegal and terrible for the retail investors.” You’re referring to Robinhood posting a bid or offer on the book and telling Citadel its theirs? I believe the “horribly illegal” bit, but why would it end up terrible for retail investors — why wouldn’t the outcome be the same? My goal here wasn’t to accurately describe the mechanics of the process; it was to describe what’s going on in a way that conveys the general idea (Robinhood privileges Citadel with information, thus giving Citadel an advantage while Robinhood gets a better idea since it can make its bids and/or offers well within the spread).

* “A better version of [5] would be Patrick McKenzie’s post” Thanks! Will link in the footnote.

LikeLike